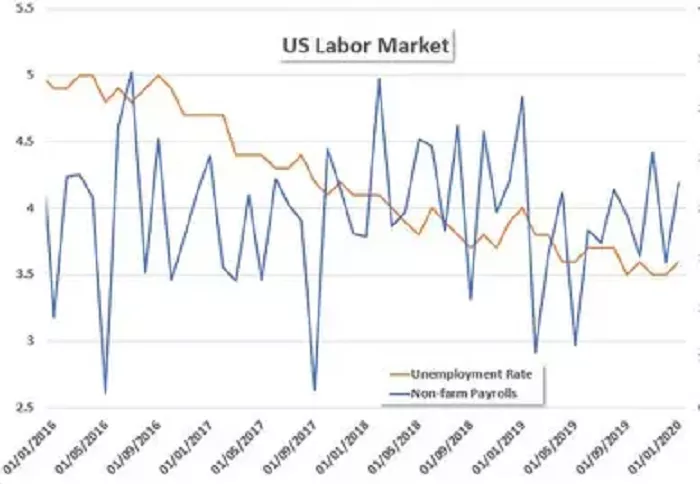

Recently, the US Department of Labor released data showing that non-farm payrolls in the United States increased by 139,000 in May, compared with the expected 130,000. The unemployment rate in May was 4.2%, in line with expectations and unchanged from the previous month.

Core Viewpoint: Employment Resilience Remains in May, Market Lowers Expectations for Interest Rate Cuts

Recruitment and Vacancies:New recruitment in the automotive and medical industries has increased, while the job gap in the information and service industries has rebounded.

As of May 2025, the average monthly recruitment plan slightly declined to 8,683, a decrease of 6,378 from the April average. In 2021, it was 127,000 (compared with 104,000 in 2019).

As of May 2025, the revised number of non-governmental sector job vacancies rose to 6.544 million, but it continued to slow down compared with the peak of over 10 million in 2022 (among which the manufacturing gap dropped to 381,000).

Non-farm Employment

The increase in employment dropped to 139,000, with the total growth rate declining to 1.1%, and the growth rates of employment in both enterprises and the government decreased.

In terms of total employment, as of May 2025, the number of new non-farm jobs increased by 139,000, among which the government decreased by 1,000 and enterprises increased by 140,000.

In terms of industry structure, education, healthcare, and hotels saw increases of 87,000 and 48,000 respectively, maintaining relatively high increments. The financial industry saw an increase of 13,000 in May, showing a significant recovery in employment increments.

The unemployment rate in May was the same as that in April, which was in line with expectations.

Salary Growth Rate

The downward revision of the growth rate provides more flexible space for policies. There is a mismatch between supply and demand between the contraction of labor supply and the still strong demand for employment by enterprises.

As of May 2025, the average weekly non-farm payroll growth rate, after revision, dropped to 3.9%, down 0.3 percentage points from before the revision in April. However, the salary growth rate remains resilient.

From the perspective of cost structure, in May, commodity production increased by 4.1%, a decrease of 0.2 percentage points. Among them, the mining industry increased by 2.1 percentage points, the construction industry by 3.7 percentage points, but the manufacturing industry increased by 4.1 percentage points. Service production rose by 3.8%, dropping by 0.3 percentage points. Among them, education and health rose by 2.5 percentage points, wholesale by 3.1 percentage points, and business services by 5.2 percentage points.

From the perspective of employment supply and demand, on the one hand, the recruitment demands of enterprises still exist, exerting a continuous pull on the labor force. On the other hand, the labor supply side has contracted significantly. The labor participation rates of whites, Hispanics or Latinos declined in May, indicating that more people are withdrawing from the labor market. In an environment where supply fails to meet demand, labor costs are passively raised, and enterprises have no choice but to attract or retain employees by increasing wages. This salary increase does not stem from productivity improvement but is the result of a mismatch between supply and demand. Therefore, it is more likely to trigger a wage-inflation spiral, increasing the difficulty for the Federal Reserve to balance its policies between inflation control and growth stability.

Related Topics: