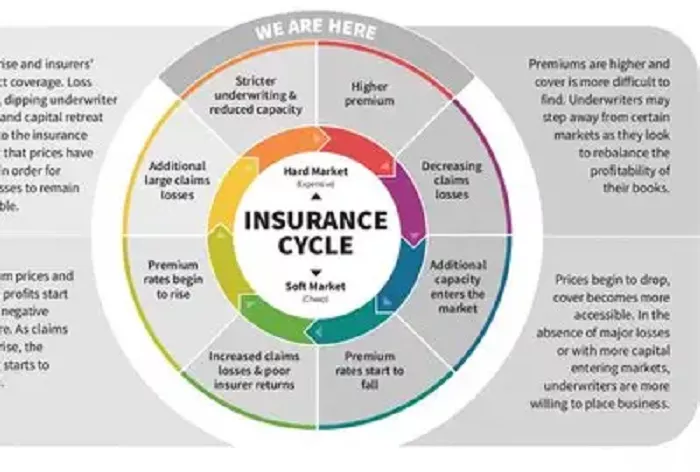

Recently, the insurance industry has been abuzz with news of an upcoming reduction in predetermined interest rates for life insurance products. This has led to the discontinuation of several savings insurance products with a predetermined interest rate of 2.5%, sparking widespread discussion. Some insurance companies have already launched new dividend insurance products with a reduced predetermined interest rate of 1.5%, down from the current market upper limit of 2%.

Key Developments

Product Discontinuation: Since June, many savings insurance products with a predetermined interest rate of 2.5% have been withdrawn from the market. Companies are now focusing on “protection + savings” to restructure their product matrices.

Market Reactions: Some consumers are choosing to wait and see, while others are determined to purchase. For example, Ms. Liu from Changsha decided to observe for a while longer after learning that the returns had decreased, while Mr. Li believes that even with reduced returns, insurance products still offer advantages over bank deposits and provide protection.

Industry Shifts: The appeal of fixed-income products is expected to decline, shifting focus towards dividend insurance. The industry is moving away from an extensive pursuit of returns to a more professional and long-term approach.

Expert Advice

Professor Zhu Junsheng from Peking University suggests that under the premise of having a long-term stable cash flow, clear protection needs, and risk tolerance, it makes financial sense to allocate funds to products with a predetermined interest rate of 2.5% or higher. However, he emphasizes that insurance is a long-term contractual arrangement, and consumers should not make hasty decisions due to “discontinuation of sales” or “reduction of the expected interest rate.” Instead, they should make rational choices based on their own cash flow planning, family responsibilities, and future spending needs.

Consumer Considerations

Industry insiders from Ping An Life Insurance Hunan Branch advise consumers to make decisions based on their actual needs and financial conditions. If there are rigid demands such as long-term savings, retirement, and education, the configuration value of insurance products still exists, and plans can be made in advance. However, if the capital demand is relatively short-term or the requirement for capital liquidity is high, such products may not be suitable. Consumers must carefully study the terms and conditions, clearly understand key information such as the product’s coverage, benefit composition, and payment methods, and avoid blindly following trends. Choosing a legitimate insurance company and a professional insurance agent is also crucial for safeguarding one’s rights and interests.

Conclusion

As the insurance market adjusts to lower interest rates, consumers face a choice: to “get on board” now or wait for better options. While there is a certain financial logic to purchasing products with higher predetermined interest rates, it is essential to consider long-term needs and financial conditions. Making informed decisions based on individual circumstances and understanding the terms and conditions of insurance products will ensure that consumers can navigate the changing market effectively and secure their financial futures.

Related Topics: